Medicare Advantage — also known as Medicare Part C — is an alternative approach to receiving your Medicare benefits. Rather than receiving coverage directly through the federal government under Original Medicare, Medicare Advantage plans are offered by private insurance companies that contract with Medicare to deliver your Part A and Part B benefits, often with additional features bundled in.

Understanding how these plans work, what they may offer, and how they compare to other Medicare options can help you make a more informed decision during enrollment.

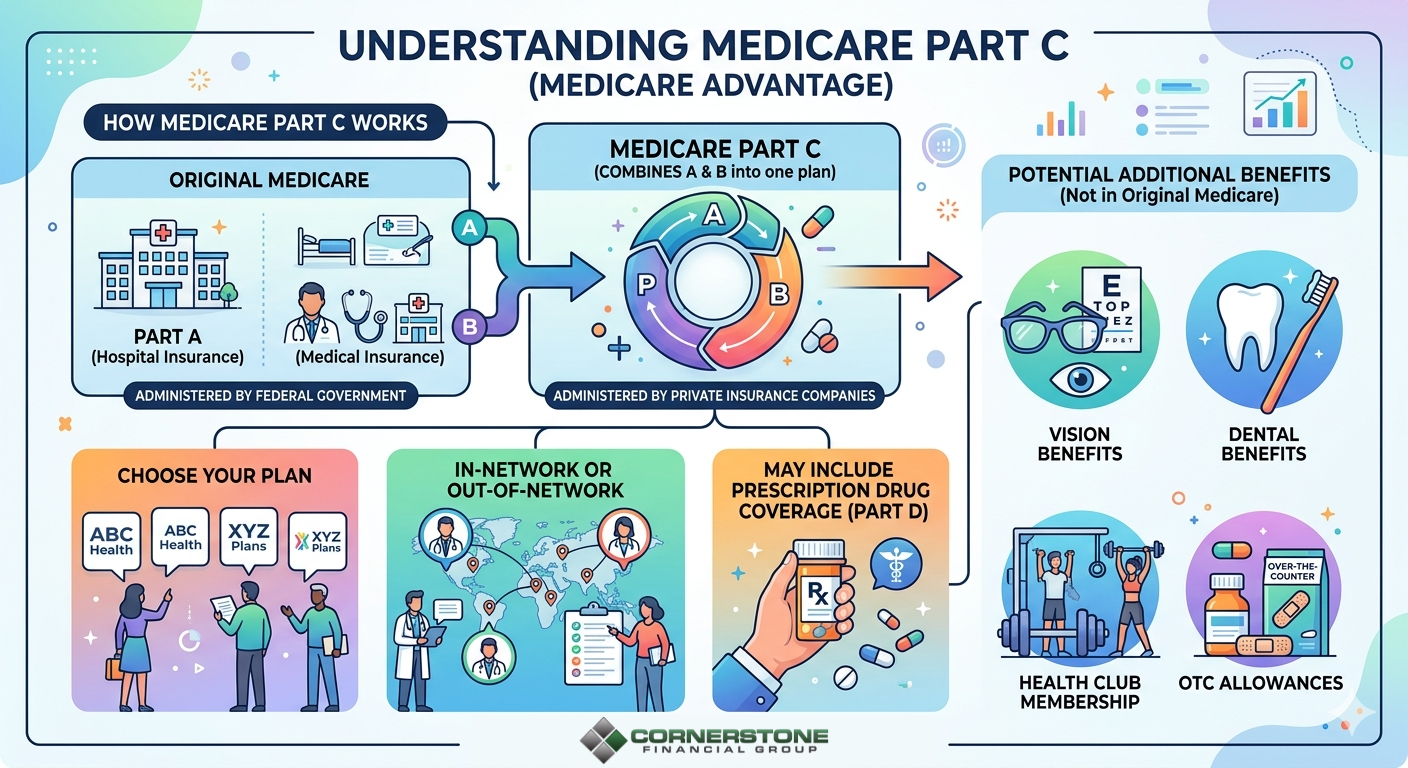

What Is Medicare Advantage?

Medicare Advantage is a type of health insurance plan that provides Medicare-covered services through a private insurer approved by the federal government. These plans are required to cover everything that Original Medicare covers (with limited exceptions), and many plans may also include additional benefits such as:

- Prescription drug coverage (Part D) — often bundled into the plan

- Vision and dental services — coverage varies widely by plan

- Hearing benefits — not covered under Original Medicare

- Wellness programs — some plans may include gym access or fitness-related benefits

- Transportation assistance — offered by select plans in certain service areas

Note: The availability and scope of additional benefits depend entirely on the specific plan and the geographic area in which you reside. Benefits are not uniform across plans.

Is Medicare Advantage Right for You?

There is no single answer to this question — and that's by design. The right Medicare coverage depends on your individual health needs, financial situation, preferred providers, and personal priorities.

Medicare Advantage may be worth exploring if you:

- Are interested in potentially consolidating multiple coverages (medical, drug, dental, vision) into a single plan

- Want to understand plans that may have different cost-sharing structures than Original Medicare

- Are comfortable receiving care within a defined network of providers

Medicare Advantage may not be the best fit if you:

- Have established relationships with specific physicians or specialists who may not participate in a plan's network

- Frequently travel or live in multiple states and need broad geographic flexibility

- Prefer the nationwide provider access that Original Medicare offers

Carefully reviewing each plan's provider network, formulary (drug list), out-of-pocket limits, and coverage rules is essential before enrolling. Past plan features are not a guarantee of future benefits, as plan details can change each year.

How Do You Enroll in a Medicare Advantage Plan?

To be eligible for a Medicare Advantage plan, you generally must:

- Be enrolled in both Medicare Part A and Part B

- Live within the plan's service area

- Not have End-Stage Renal Disease (ESRD) — though this restriction has been modified under recent federal rules; confirm current eligibility requirements with a licensed agent or Medicare directly

Key enrollment windows include:

- Initial Enrollment Period (IEP): When you first become eligible for Medicare, typically around your 65th birthday

- Annual Enrollment Period (AEP): October 15 – December 7 each year, during which you may switch, join, or drop a Medicare Advantage plan

- Medicare Advantage Open Enrollment Period (OEP): January 1 – March 31, during which you may switch to a different Medicare Advantage plan or return to Original Medicare

- Special Enrollment Periods (SEPs): Available in certain qualifying life circumstances, such as retiring and losing employer group health coverage

Missing an enrollment window may limit your options. It's advisable to be aware of your personal eligibility dates and plan accordingly.

Medicare Advantage vs. Medicare Supplement Insurance: An Important Distinction

These two types of coverage are frequently confused — and the difference is significant.

| Medicare Advantage | Medicare Supplement (Medigap) | |

|---|---|---|

| How it works | Replaces Original Medicare with private plan coverage | Works alongside Original Medicare to help cover cost-sharing gaps |

| Network restrictions | Typically yes — HMO or PPO networks | Generally no — use any provider that accepts Medicare |

| Additional benefits | May include drug, dental, vision, and more | Does not typically include drug or vision/dental coverage |

| Premium structure | Often lower monthly premiums; cost-sharing at point of service | Higher monthly premiums; lower or no cost-sharing at point of service |

Neither option is universally better. The right choice depends on how you use healthcare, your financial situation, and your priorities around flexibility versus bundled benefits.

Questions to Ask Before You Enroll

Before selecting any Medicare Advantage plan, consider asking:

- Are my current doctors and preferred hospitals in this plan's network?

- Are my prescriptions covered under this plan's formulary, and at what cost?

- What is the plan's maximum out-of-pocket limit for covered services?

- Does the plan require referrals to see specialists?

- What happens if I need care outside the plan's service area?

- Have I compared this plan against other options available in my ZIP code?

Plan details — including premiums, cost-sharing, networks, and additional benefits — change annually. Reviewing your plan options each Annual Enrollment Period is strongly recommended.

Why May Is Still the Right Time to Think About Medicare

If you're reading this in May, you might notice that no active Medicare enrollment period is currently open — and that's exactly the point.

Medicare decisions made during enrollment periods are shaped by the groundwork laid months before. Beneficiaries who wait until October to start thinking about their coverage often find themselves rushed, comparing plans under deadline pressure without a clear sense of what they actually need or what's changed since last year.

May offers something valuable: time without urgency. It's a natural moment to take stock of your healthcare needs, review how your current coverage has performed, and consider whether your Medicare plan still fits where you are in your retirement.

For those approaching retirement, this timing matters even more. Medicare is one of the larger healthcare cost variables in any retirement income plan. Understanding how different coverage structures — Medicare Advantage, Medicare Supplement, Part D — interact with your overall financial picture is best done thoughtfully, not in the final days of an enrollment window.

Some questions worth reflecting on now:

- Has your health situation or prescription needs changed since you last reviewed your plan?

- Are you approaching 65 and unsure when or how your Medicare coverage should begin?

- Is your current plan still the most appropriate fit, or have your priorities shifted?

- How does your Medicare coverage fit within your broader retirement income and healthcare budget?

There's no enrollment action required today — but there may be planning conversations worth starting.

Medicare Enrollment Windows for 2026

Medicare enrollment for 2026 is divided into specific windows based on your personal circumstances. It's important to be aware of which window applies to your situation, as enrolling outside an eligible period may affect your coverage options.

Annual Enrollment Period (AEP): October 15 – December 7 During this window, Medicare beneficiaries may join, switch, or drop a Medicare Advantage or Part D prescription drug plan. Changes made during AEP generally take effect January 1 of the following year.

Medicare Advantage Open Enrollment Period (OEP): January 1 – March 31 If you are already enrolled in a Medicare Advantage plan, this period allows you to switch to a different Medicare Advantage plan or return to Original Medicare (with or without a standalone Part D plan). You may not use this period to switch from Original Medicare to a Medicare Advantage plan.

Initial Enrollment Period (IEP): Year-round, based on individual eligibility Your IEP is a 7-month window centered around the month you turn 65 (or when you become eligible due to disability). Enrolling promptly may help you avoid potential late enrollment penalties.

Special Enrollment Periods (SEPs): Year-round, based on qualifying life events Certain circumstances — such as losing employer-sponsored coverage, relocating out of a plan's service area, or qualifying for a low-income assistance program — may trigger a Special Enrollment Period. SEP eligibility and duration vary by circumstance.

Enrollment period rules are subject to change. Always verify your eligibility dates and applicable windows with a licensed insurance professional or directly through Medicare.

Speak With a Licensed Agent

Reviewing your Medicare options — particularly as the Annual Enrollment Period approaches — can feel like a lot to navigate on your own. Our licensed Medicare agent, Danielle McKenna, may be able to help you understand the options available in your area, review your current coverage, and discuss how different plans may align with your healthcare needs.

Danielle McKenna

Financial Paraplanner Qualified Professional (FPQP®)

CA License #0D97816 | NV License #3654433

To schedule an appointment:

- Phone: 530-672-1703

- Email:info@cfgstrategies.com

Taking time to review your options before enrollment deadlines may help you make a more informed coverage decision for 2026. We encourage you to reach out with any questions.

This article is intended for educational and informational purposes only and does not constitute financial, legal, medical, or insurance advice. This content should not be construed as a recommendation or guarantee of any specific plan, benefit, or outcome. Plan availability, benefits, premiums, costs, and coverage details vary by location, carrier, and plan year and are subject to change annually. Not all plans are available in all areas. Consult a licensed insurance professional and carefully review plan documents, including the Evidence of Coverage (EOC) and Summary of Benefits, before making any enrollment decisions. Not endorsed by or affiliated with the Centers for Medicare & Medicaid Services (CMS), the Social Security Administration, or any other government agency. For official Medicare information, visit Medicare.gov or call 1-800-MEDICARE (1-800-633-4227).This content was generated utilizing the help of AI research and is intended for informational purposes only. Please consult a qualified professional for personalized advice. Sources: Medigap Select. “Medicare Advantage.” Medigap Select, https://medigapselect.com/medicare-advantage/